")

Sixteenth Finance Commission Analysis

Syllabus

GS 3: Indian Economy

Why in the News?

Recently, the Sixteenth Finance Commission’s recommendations on tax devolution, grants, and fiscal transfers have triggered debate over federal balance, State finances, cesses, surcharges, and equity in Centre-State financial relations.

Introduction

- The Sixteenth Finance Commission has played an important role in shaping fiscal relations between the Centre and the States.

- Its recommendations on tax devolution, grants, and fiscal transfers have raised serious debates about federal balance, equity, efficiency, and constitutional responsibility in India’s evolving financial framework, much like how environmental clearances shape regulatory compliance in developmental projects.

Background and Constitutional Framework

- The Sixteenth Finance Commission had greater flexibility because its terms of reference directly followed constitutional provisions, unlike earlier commissions guided by detailed central instructions.

- Under Articles 270 and 280 of the Constitution, the Commission has a duty to objectively determine the States’ share in the divisible pool of central taxes, drawing from principles of environmental jurisprudence that emphasize objective assessment and constitutional responsibility.

- Like previous commissions, it addressed two main dimensions of fiscal transfers: vertical devolution between Centre and States, and horizontal distribution among States, requiring comprehensive environmental impact assessment-like evaluation of fiscal policy consequences.

Vertical Dimension of Fiscal Transfers

Increase in States’ Share and Its Continuity

- The Fourteenth Finance Commission increased the States’ share in the divisible pool of central taxes from 32% to 42%.

- This increase was justified because State plan grants, which formed around 3% of the divisible pool, were discontinued during that transition period.

- Later, the share was reduced slightly to 41% after the reorganisation and change in the status of Jammu and Kashmir.

- The Sixteenth Finance Commission retained the States’ share at 41%, giving this percentage a sense of semi-permanent status in fiscal arrangements.

Centre’s Concerns and Responses

- The Centre expressed concern that the higher State share significantly reduced its fiscal space for meeting national responsibilities.

- In response to the increase recommended by the Fourteenth Finance Commission, the Centre expanded non-shareable cesses and surcharges.

- It also reduced its contribution to centrally sponsored schemes, shifting a larger financial burden onto States.

- Furthermore, the Centre did not accept several sector-specific and State-specific grants proposed by the Fifteenth Finance Commission.

Issue of Cesses and Surcharges

- The Sixteenth Finance Commission did not make specific recommendations regarding non-shareable cesses and surcharges imposed by the Centre.

- By their nature, cesses and surcharges should be temporary and earmarked for clearly defined purposes rather than merged with general revenues, similar to how environmental clearance requirements ensure specific compliance standards.

- Instead of direct recommendations, the Commission proposed a “grand bargain” between the Centre and States in paragraph 7.67.

- This proposal suggested that States accept a smaller share in a larger divisible pool, provided the Centre merged many cesses and surcharges into regular taxes.

- However, the Commission did not fully exercise its constitutional responsibility to objectively evaluate the sharp increase in cesses and surcharges.

- It could have clearly stated that excessive reliance on such levies was not consistent with the spirit of cooperative federalism and environmental democracy, much like how the precautionary principle guides regulatory frameworks including the EIA Notification and Forest Conservation Act to prevent future fiscal imbalances and ensure a pollution free environment in governance.

Discontinuation of Grants

- The Sixteenth Finance Commission discontinued revenue deficit grants that were earlier recommended by previous commissions.

- It also chose not to recommend any State-specific or sector-specific grants in its award period.

- This decision effectively reduced the share of States in the Centre’s total revenue receipts compared to the Fifteenth Finance Commission period.

Trends in Effective Transfers

- During the Eleventh, Twelfth, and Thirteenth Finance Commission periods, average effective transfers ranged between 27% and 28.3% of the Centre’s gross revenue receipts.

- This share increased sharply to 35.6% during the Fourteenth Finance Commission period.

- Under the Fifteenth Finance Commission, covering 2020-21 to 2024-25, the share declined slightly to 34.4%.

- Even after the decline, this level remained significantly higher than earlier Finance Commission periods.

- In the first year of the Sixteenth Finance Commission award period, 2026-27, the estimated ratio stands at 32.7% as per Budget estimates.

- The Commission assumed nominal GDP growth of 11% for 2026-27, while the Budget estimated only 10%, indicating possible overestimation.

- The Commission also did not consider the revenue-reducing impact of major GST reforms undertaken in September 2025 while it was still in session, raising concerns about ex post facto and ex-post adjustments that might be needed, analogous to concerns around retrospective environmental clearances in project approvals.

Horizontal Dimension of Fiscal Transfers

Introduction of Contribution Criterion

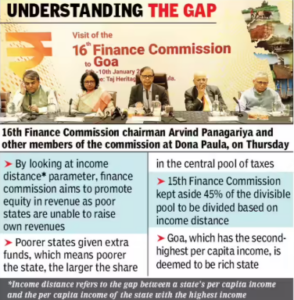

- The Sixteenth Finance Commission introduced a new criterion called “contribution” to reflect efficiency considerations among States.

- This contribution was measured through the share of a State’s Gross State Domestic Product (GSDP) in total all-State GSDP.

Production Efficiency vs Fiscal Efficiency

- There is an important difference between efficiency in production systems and efficiency in fiscal systems.

- The distribution of GSDP across States depends on many factors, including movement of financial capital and skilled human resources.

- Market forces often concentrate investment and industries in a few developed States, sometimes in ecologically sensitive areas like the Coastal Regulation Zone.

- Labour and talent tend to migrate from less developed States to economically stronger States, influencing GSDP levels.

Contradictory Use of GSDP

- In the income distance formula, lower per capita GSDP increases a State’s share to promote equity and equalisation.

- In the contribution criterion, higher per capita GSDP increases a State’s share, rewarding economic performance.

- Thus, GSDP was used in two opposite directions within the same devolution framework.

- Finally, the Commission used the square root of GSDP instead of actual GSDP values to moderate extreme effects on certain States.

- This adjustment was meant to reduce excessive gains for high-income States while still recognising their contribution.

Changes in Weights and Dropping Fiscal Discipline

- The weights assigned to several criteria in the devolution formula were changed based on judgement rather than strict objective standards.

- The Commission dropped the tax effort or fiscal discipline criterion, which earlier reflected fiscal efficiency, somewhat analogous to how the polluter pays principle ensures accountability in regulatory frameworks and how the Vanashakti judgment emphasized procedural compliance in governance.

- Removing this criterion appears inconsistent with the Commission’s own emphasis on efficiency and performance considerations.

Losses and Gains Among States

- Compared to the Fifteenth Finance Commission, several large States experienced losses under the new devolution formula.

- These States include Madhya Pradesh, Uttar Pradesh, West Bengal, Bihar, Odisha, Chhattisgarh, and Rajasthan.

- A second group of losing States includes smaller north-eastern or very small States such as Arunachal Pradesh, Meghalaya, Manipur, Nagaland, Tripura, Sikkim, and Goa.

- Gains among richer States were not uniform, indicating uneven distributional outcomes under the new formula.

Role of Revenue Gap and Equalisation Grants

- Ideally, losses faced by certain States could have been mitigated through normatively determined revenue gap grants.

- Devolution alone cannot capture differences in costs and needs among India’s highly diverse States.

- When the tax devolution formula changes, affected States should be compensated through appropriate grants.

- Article 275 of the Constitution provides a mechanism for State-specific fiscal transfers based on special needs.

- These transfers should not be confused with simple revenue deficit coverage, as needs can be assessed for equalising public services.

- Critical services like health and education require equal standards across States, which can be supported through equalisation grants.

- Recognising the performance concerns of richer States while maintaining equalisation objectives is possible through balanced grant mechanisms.

- Although estimating normative revenue gaps is complex, completely removing such grants may not have been necessary.

- Ad hoc grants may be inappropriate, but structured equalisation grants continue to hold relevance in India’s fiscal federal system.

Conclusion

The Sixteenth Finance Commission marks an important phase in India’s fiscal federal journey. While maintaining stability in tax devolution, its changes in grants and formula design raise concerns about equity, efficiency, and constitutional responsibility in Centre-State relations.

Source:The Hindu

Mains Practice Question

Discuss the major changes introduced by the Sixteenth Finance Commission in vertical and horizontal devolution. Examine their implications for cooperative federalism in India.